Table of Contents

Why in 2025 cards are only 40 percent of an ad account’s payment signature

In 2025 advertising platforms no longer see the card as the main reliability marker. It still serves as a source of funds, but its weight in the overall risk score has dropped to around forty percent. The rest comes from the context in which the card is used. Platforms look at it as a combined fingerprint, where the card is just one of several dozen variables.

How Meta and TikTok evaluate advertiser risk score: the role of payment signature, device graph, timezone consistency, and behavior velocity

Risk scoring in Meta and TikTok systems is built not around individual transactions but around the payment signature. The system analyzes device stability, authorization history, account connections in the device graph, and how well ad actions match the expected timezone. Timezone consistency is now seen as a signal that the person running the campaign actually belongs to the region listed in the business profile. Behavior velocity completes the picture. If budget changes happen faster than expected models allow, the platform reduces trust and starts imposing stricter authorization requirements. This shifts the focus from the card itself to the advertiser’s overall behavior.

Why optimizing BIN no longer guarantees approval: the card is now a trigger, not the main factor

Agencies used to pick BINs mainly to boost approval rates. In 2025 that stopped working. The issuing bank could be perfect, but if account behavior clashes with platform metrics, the card becomes a trigger. It prompts a review but no longer determines the outcome. A carefully chosen BIN cannot make up for a wrong IP, unstable device connections, or unexpected velocity spikes.

New criteria for choosing a provider

A new factor has emerged in selecting a provider. If a service allows timezone settings, IP group management, cookie persistence, and device synchronization with authorizations, its cards perform better even with a neutral BIN. Agencies no longer choose an issuer based only on country and MCC because the payment context has become more important than the card itself.

Card characteristics agencies need in 2025 for ad payments

Agency requirements have changed. Now it’s not just card details that matter, but also how well the card integrates into a stable payment context.

- Device aware cards: services that give control over timezone, IP consistency, cookie persistence, and multi seat device linking

Modern services must support device aware logic. Agencies get control over timezone so that all payments look natural to the platform’s model. IP consistency maintains a single network profile for the team. Cookie persistence and multi seat device linking preserve browser history across multiple employees, forming a stable fingerprint.

- Predictable issuer risk profile: stable BIN pools, no network changes, no unexpected regional reroutes

Issuers must ensure BIN stability. Banks occasionally change network routing, which affects the risk module. If a BIN suddenly routes through a different region, ad platforms detect a mismatch and decline payments. Agencies choose providers that minimize such network fluctuations.

- API level control: managing authorization flow, webhooks for decline reasons, and the ability to adjust spend velocity in real time

API control is now mandatory. Agencies need access to decline reasons and the ability to manage authorizations without operator involvement. Spend velocity parameters must adjust dynamically to align account behavior.

- Anti-fraud compatibility: how the card fits into Meta and TikTok models

Major ad platforms require low latency authorizations. The card must respond quickly and consistently. Correct AVS, stable CVC lifecycle, and predictable issuer behavior create a high trust score. If these elements fail, payments drop regardless of the BIN.

Top 3 services ideal for modern advertising conditions

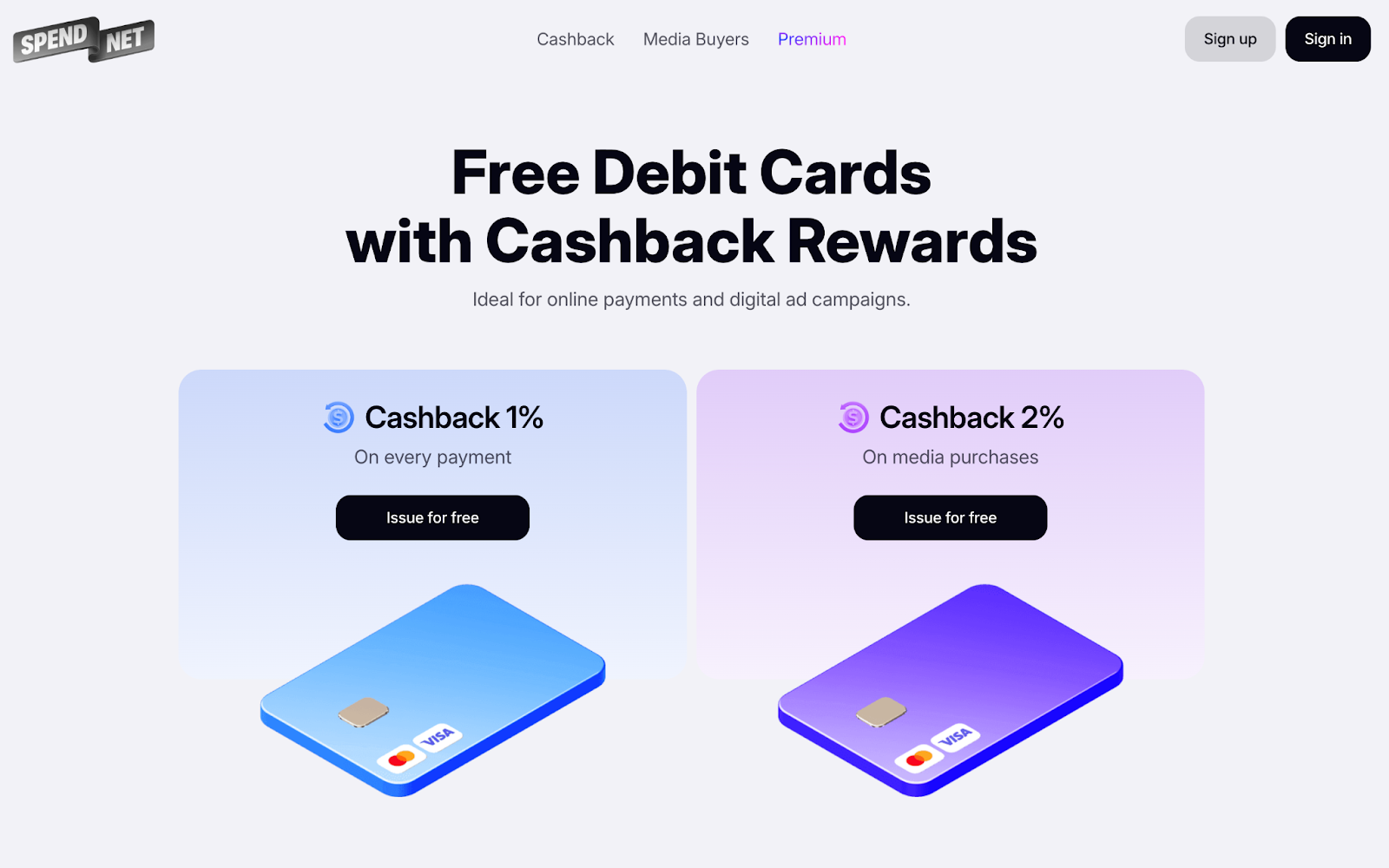

- Spend.net

Spend.net relies on a pool of twenty BINs, including six unique ones, providing a wide range of signatures for ad accounts. Support for Visa and Mastercard keeps cards neutral regarding global transaction routing.

There are no limits on the number of cards, reducing velocity spikes when creating new cards and allowing each ad campaign to have its own independent payment context. Team features let roles be assigned and cards linked to specific traffic streams, lowering the risk of device to card desynchronization, especially in agency structures.

Cards support 3D Secure, which adds a behavioral signal of a normal challenge flow for some ad platforms. Spend.net does not intervene in authorizations, creating a stable response pattern without extra hops.

Crypto top-ups like USDT and BTC reduce delay risks but only affect operations, not the trust score.

The biggest operational advantage is zero fees for transactions, declines, refunds, and withdrawals. This minimizes balance noise and simplifies velocity forecasting. Users control top-up fees, which start around two percent on average.

24/7 live chat support, CSV/XLS reports, and 2 percent cashback automatically applied to ad payments make the platform appealing for teams seeking full expense transparency and simple operations without bureaucracy. Spend.net fits agencies prioritizing predictable expenses and the ability to multiply cards without changing BIN signatures.

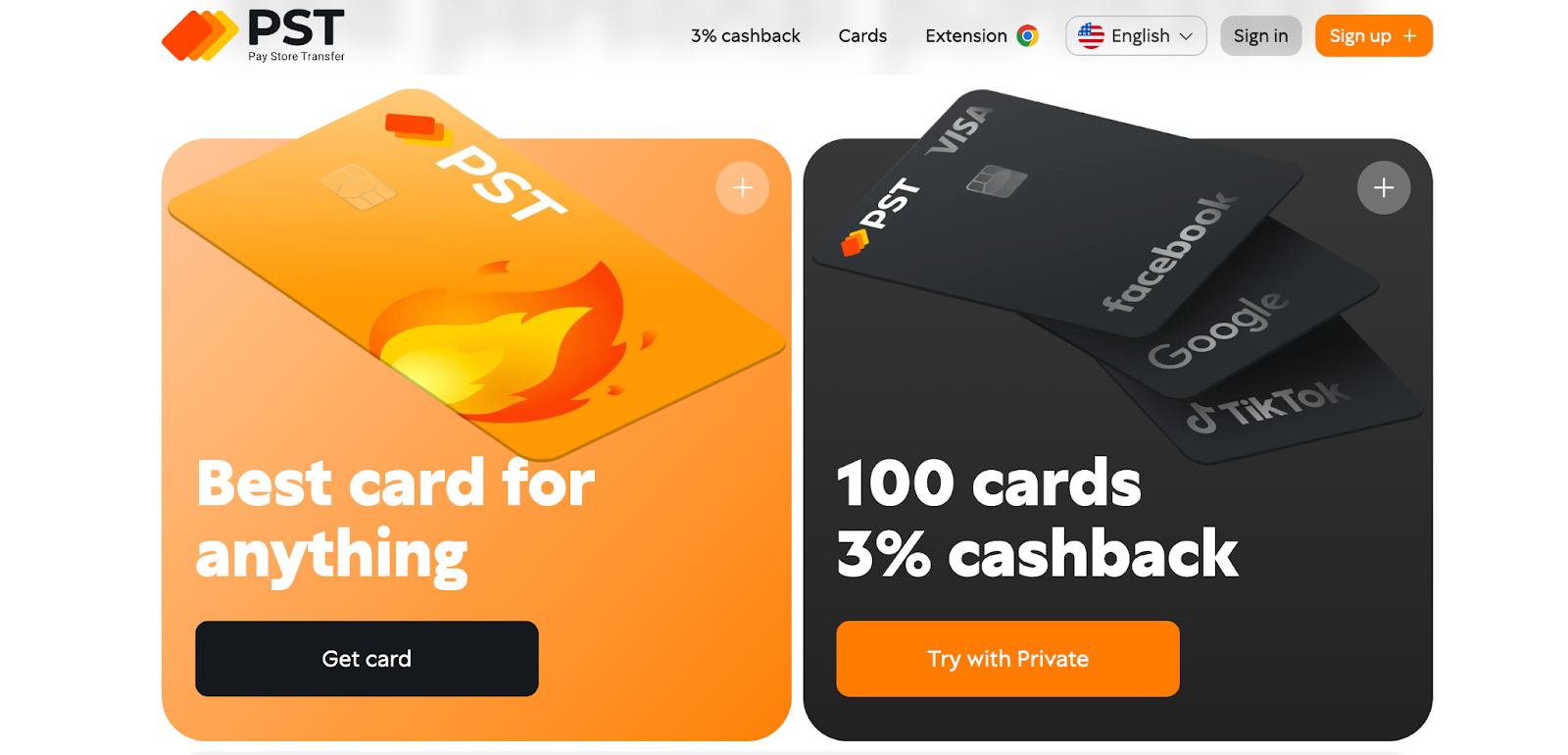

- PSNET

PST.NET uses over twenty-five BINs covering the US and Europe. This wide signature range reduces the chance of hitting narrow risk segments in Meta and TikTok.

Cards are internally segmented per platform. For example, BINs optimized for MCC 7311 and an extra Ultima card covers non-core expenses, relieving the main payment context. Behavioral data is visible in the BIN checker: average spend, approval rates, and billing thresholds for each BIN, helping agencies predict payment signatures in advance.

Team features include subaccounts, limit settings, and auto top-up. 3DS and two-factor authentication provide a smooth challenge flow. Top-ups are available in eighteen cryptocurrencies, SWIFT, and SEPA. USDT deposits for new users are free.

PST Private provides up to 100 free cards monthly, reducing the need to recreate cards and minimizing device to card anomalies. Cashback is 3 percent for ad spend, and top-up fees are lower. No turnover confirmation is needed, making it suitable for teams of any size.

Cards behave predictably in terms of velocity, since the service does not impose its own transaction fees. PSTNET supports multichannel communication through Telegram, WhatsApp, and live chat, with iOS and Android apps. Cashback accrual for ad spend is displayed in real time.

PSTNET fits agencies building their own risk pipelines and needing stable BIN pools, operational predictability, and automation.

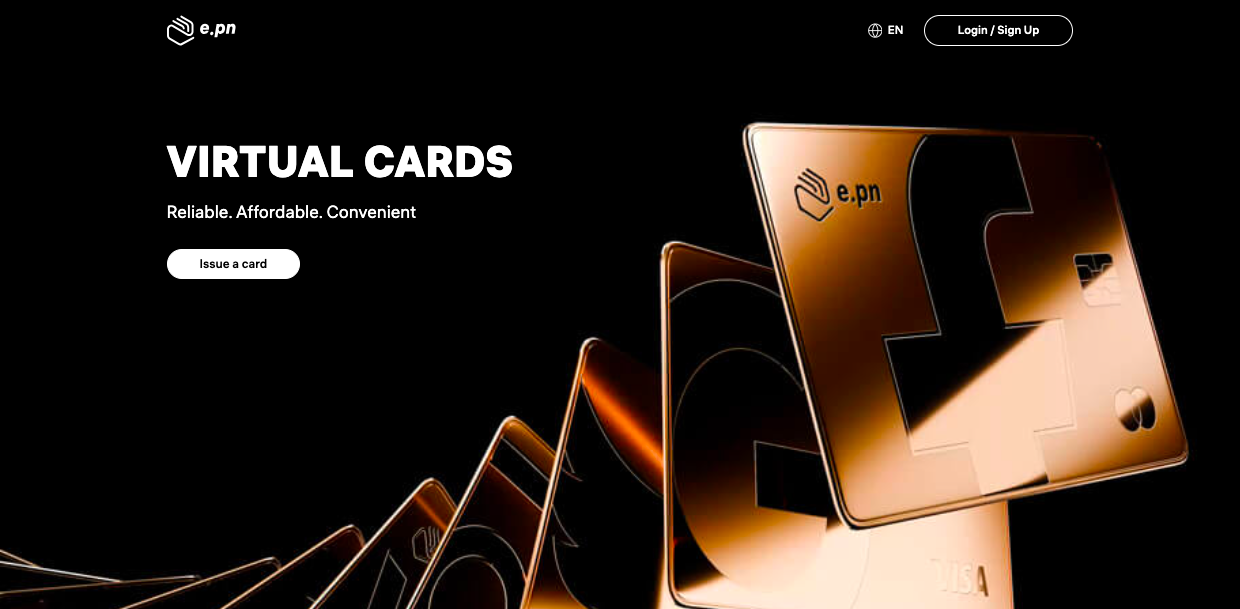

- EPN

EPN has more than twenty BINs. The starter set includes seven BINs in the US and Brazil, with more opening as spend grows, making the signature adaptive for account development.

All cards are USD, reducing conversion spikes and billing noise on Meta, Google, and TikTok. Fees apply for transactions, declines, and service, and top-up fees range from zero to thirteen percent, potentially creating variable velocity.

Teams get full control: team leads, card allocation, unlimited card creation, supporting structured payment signatures. 3D Secure improves trust trajectory on sensitive platforms. Top-ups are possible via crypto, wire transfers, Capitalist, and Payoneer. Cards support Visa and Mastercard.

Card issuance and renewal fees are 2–4 dollars, with a 3 percent fee on non-USD transactions. Support is available via tickets, chat, email, and Telegram.

EPN suits agencies working across wide geographies and needing flexible card signatures based on spend. It provides a large BIN range but requires careful management of expenses and top-ups.

How ad platforms interpret the card: mechanics usually hidden

Ad platform card evaluation algorithms have become more sophisticated and focus on contextual interpretation. The card is not assessed on its own but in connection with advertiser behavior.

- BIN level signals: geo BIN scoring, BIN types, issuer country risk

The BIN still provides multiple signals. The system considers the issuer’s region and its risk level. Some countries get lower scores due to frequent spam schemes, even if the card is fully legal. BIN type matters too. Commercial BINs tend to yield a higher trust score. Debit BINs can trigger stricter checks due to unstable limits. Geo BIN scoring is now a separate parameter determined in combination with IP and timezone.

- 3DS flow as a behavioral marker: how frequent 3DS challenges affect trust score

3DS is no longer just a security step. Frequent challenges signal unstable advertiser behavior. If a card constantly requires verification, the platform interprets this as a risky client or suspicious authorization. Trust score drops inevitably. Some agencies avoid cards with aggressive 3DS because the models often trigger checks on every payment change.

- MCC plus issuing bank heuristics: why the same MCC behaves differently across issuers

Ad MCCs are interpreted in complex ways. Even if the MCC is identical, banks apply their own fraud heuristics. One bank may see ad payments as low risk, another as high. This affects authorization even before the transaction hits platform models. That’s why identical BINs can behave differently.

- Impact of velocity patterns: limits, burst spend, time of day irregularities

Velocity patterns are a key signal of advertiser behavior. If budgets suddenly spike several times, transactions only go through if other metrics align. Irregular timing patterns cause issues. Payments outside historical patterns reduce trust score. Platforms treat daily and monthly limits as behavioral models, not technical card parameters.

How to choose a card provider: checklist for agencies on risky platforms

The provider has become a risk management partner, not just an issuer.

- Primary level: issuing bank, geo BIN, pooling stability: Agencies need predictability. Issuers must ensure stable BIN routing and consistent regional settings.

- Behavioral level: device sync support, timezone locking, IP policy: It’s critical to enforce timezone locking, configure IP groups, and maintain fingerprint consistency.

- Technical level: API stability, 3DS flow control, predictable authorizations: Services should provide tools to manage 3DS and be predictable in authorizations. Any delay causes platform issues.

- Operational level: fast card replacement without changing BIN signatures, quarantine for new devices: Services must allow card replacement within a BIN pool to maintain the payment signature. Device quarantine helps preserve account trust.

Conclusion: the card is no longer the center of payment, context is the new infrastructure

The more accurately you understand BIN origin and track the connection between geo, bank type, MCC risks, and approval history, the less budget is lost on declined payments and blocked cards.

Your results depend on the virtual card service you use, the transparency of its BINs, the analytics it provides, and whether it allows control over fees, limits, teams, and security.

For example, SPEND.net focuses on free cards, zero operational fees, and user-controlled top-up fees. Its 20 BINs (6 unique), 3DS support, unlimited cards, CSV/XLS reporting, and real-time cashback display make it attractive for teams seeking transparent spending and simple operations.

PSTNET targets large-scale media buying: over 25 BINs from the US and Europe, BIN analytics (spend, approval rate, billing thresholds), up to 100 free cards per month, zero-fee deposits, 3 percent PST Private cashback, auto top-up, subaccounts, wide funding methods, and communication via Telegram/WhatsApp. This blends analytics, flexibility, and scalability.

EPN offers access to a large BIN range that works well in Facebook Ads, Google Ads, and TikTok. BIN growth depends on spend, providing predictable billing. Fees are higher, but the service offers fine-tuned limits, team lead functions, detailed analytics, transaction filters, Excel exports, and mobile apps for remote work. This suits agencies willing to pay for advanced control.

However, if a provider does not guarantee fingerprint integrity and IP stability, any card advantage disappears. The issuer can provide a good BIN, but without proper payment sync, cards lose viability. Security today is built around environment consistency, not just card details.

Overall, payment reliability on ad platforms is a combination of three things: correct BIN checks, choosing the right card service, and disciplined payment practices.